Planning for retirement is one of the most crucial steps you can take towards securing your financial future. Whether you’re just starting your career or nearing the end of your working years, understanding the nuances of retirement planning can make a significant difference in your quality of life post-retirement.

In this post, we examine Retirement 101 and the various types of retirement accounts and how TRADEway can assist you in planning for your retirement. By empowering yourself with knowledge and strategies, you can navigate the complexities of retirement planning with confidence and pave the way for a potentially secure and fulfilling retirement.

Why Are There So Many Types of Retirement Accounts?

Employer-Sponsored Accounts

- 401(k): A common employer-sponsored retirement plan

- 403(b): Designed for employees of public schools and certain tax-exempt organizations

- Thrift Savings Plans (TSPs): Available to federal employees and members of the uniformed services

- Pensions: Traditional retirement plans offering fixed monthly payments

If you work for a company that offers a retirement package, there’s not much choice you have in what kind of option you can choose and select. It’s going to be what your employer is offering and you have the choice whether you want to participate in it or not.

In this example, we’re going to be talking about a 401k, which would be considered a defined contribution plan versus what would be a defined benefit plan.

A defined benefit plan would be like a pension plan that pays out a certain amount each month. You can receive a percentage of your highest grossing salary upon your retirement.

A 401k plan is defined by how much has been contributed into it. You would personally make pre-tax or post-tax contributions to your retirement account from your paycheck. Additionally, many employers will also match your contribution up to three to five percent.

Now if you’re putting in post-tax contributions to your 401K, meaning you’ve paid the taxes up before depositing to your account, your employer may contribute pre-tax, meaning you’re going to have to pay taxes on the earnings from that when you take the distribution.

Individual Retirement Accounts (IRAs)

- Traditional IRA: Contributions may be tax-deductible, with taxes paid upon withdrawal

- Roth IRA: Contributions are made with after-tax dollars, allowing for tax-free withdrawals in retirement

So what if your employer doesn’t offer retirement benefits or maybe you’re self employed?

There are a few options.

A traditional IRA allows you to contribute the pre-tax money, so that could potentially reduce the tax liability for you that year, by reducing your earnings for that year. There’s a max contribution of $7,000 ($8,000 if you’re 50 or older). Taxes are paid when you take distributions out.

These limits get adjusted every year. The information in this post contains the current 2024 information.

The next one is the Roth IRA. The interesting thing about your Roth IRA is that you’re contributing the post-tax money, meaning you’ve already earned the income, you’ve paid taxes on it, you can contribute the $7,000 ($8,000 if you’re older than 50), but everything that would grow in that account is actually going to be tax free.

So it’s tax free upon distribution and there are no required minimum distributions. Now there are eligibility restrictions when it comes to income. With higher earners it phases down or you may not be able to contribute to this at all, which is different than the Roth 401k, which you can continue to contribute to.

Note: If you are in a higher tax bracket right now, the more you can save, and invest it tax deferred into your retirement accounts, that amount is deductible from your gross annual income. Consult with your CPA or tax professional for more information.

How Can Tradeway Help You Prepare For Retirement?

At TRADEway, we care about you, we care about your family, and we’re trying to provide you with support for some of the existing retirement alternatives. You don’t have to go through a financial crisis with a buy and hold mentality.

Maybe you would like some different options that are not available in your traditional 401k programs because of the limitations that exist in those programs.

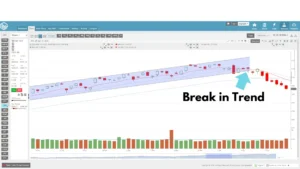

If we go into a recession, on average, the bear markets are at least 34 percent down and you don’t want to see a 34% decline in your portfolio.

Can TRADEway help manage your portfolio for you in such a way that it helps protect your funds during those significant downturns?

Imagine this: there is a hurricane coming. What do you do? You get prepared for the hurricane before the hurricane hits. We know these economic hurricanes come. So, if you were prepared for the economic hurricane, you boarded up your portfolio’s windows, and you will survive through that economic hurricane with minimal scratches. You know, you had a little bit of damage in the yard, but your house was fine and everything came through with just very nominal damage.

That’s what we do at Assisted Managed Portfolios by TRADEway – AMPT.

As licensed traders – Investment Advisory Representative (IAR), the AMPT team can get in and out of positions as the market changes. And it’s known as discretionary trade authority.

This is a big advantage of working with AMPT, because traditional financial advisors don’t have or don’t want discretionary trade authority. They’re going to meet with you once every six months or a year, or in the case of your 401k, probably never.

That’s not the way the AMPT program works. You give AMPT the discretion to change your allocations at any moment.

AMPT Portfolio Management Options

Assisted Managed Portfolios by TRADEway – Advanced Investment Management (AIM )

TRADEway created a program that mirrors that philosophy and it’s called AIM, Advanced Investment Management, and it leverages the biblical concepts from Ecclesiastes and from the book of Ezekiel to create a diversified portfolio That’s designed for more of a long-term approach with more diversification and more safety, and our team does that for you.

We are in and out of ETFs that mimic the sectors of the economy. We’ll change the allocations when we’re not confident of what the market’s doing, we’ll pull back on allocations. We’ll be more in cash getting that current 4.287 percent. When we’re confident in a specific sector, we’ll put more money into that sector as opposed to other sectors.

And it takes just a few clicks of the button for our team to invest those for you. And it’s a pretty powerful way for us to do things that your 401k is not going to do. Most of the time, they’re going to leverage mutual funds, while you don’t even know what those funds are or how they’re invested. With us, we’re going to be in and out of those positions based on what we see happening inside the economy.

Assisted Managed Portfolios by TRADEway – Ultra Portfolio (UP)

The Ultra Portfolio program is active trading with a small portion of your money.

The Ultra Portfolio is more focused on short term trades. We get in and get out of trades and try to make a little higher returns on a smaller portion of your money by taking more risk.

In this portfolio, we utilize index-based financial instruments, ETFs, stocks and stock options, and trade based upon market cycles and short-term time frames. Let TRADEway help you with managing a portion of your funds (more aggressively) with a trader’s mindset!

At TRADEway, our AMPT team is dedicated to helping you navigate the intricacies of retirement planning and portfolio management. With our team, you can explore a range of options tailored to your specific financial goals and risk tolerance. Whether you’re looking to diversify your investments, maximize your savings, or simply gain a deeper understanding of your retirement strategy, our team is here to provide you with personalized insights and guidance.

Don’t leave your financial future to chance—contact the TRADEway AMPT team today to learn how we can assist you in preparing your portfolio for retirement. Get started on your journey to financial peace of mind by reaching out to us now.